What a Cash Flow Statement is

The Cash Flow Statement (CF) shows where actual cash came in and where it went out during a period. It complements the P&L (which shows profit on an accrual basis) and the Balance Sheet (which shows balances at a point in time).

The simple question it answers: how much cash did the business generate or consume?

A profitable business can run out of cash if customers pay slowly or if it's funding inventory. A money-losing business can have plenty of cash if it's drawing down savings. The Cash Flow Statement is what tells you which scenario you're in.

How to run it

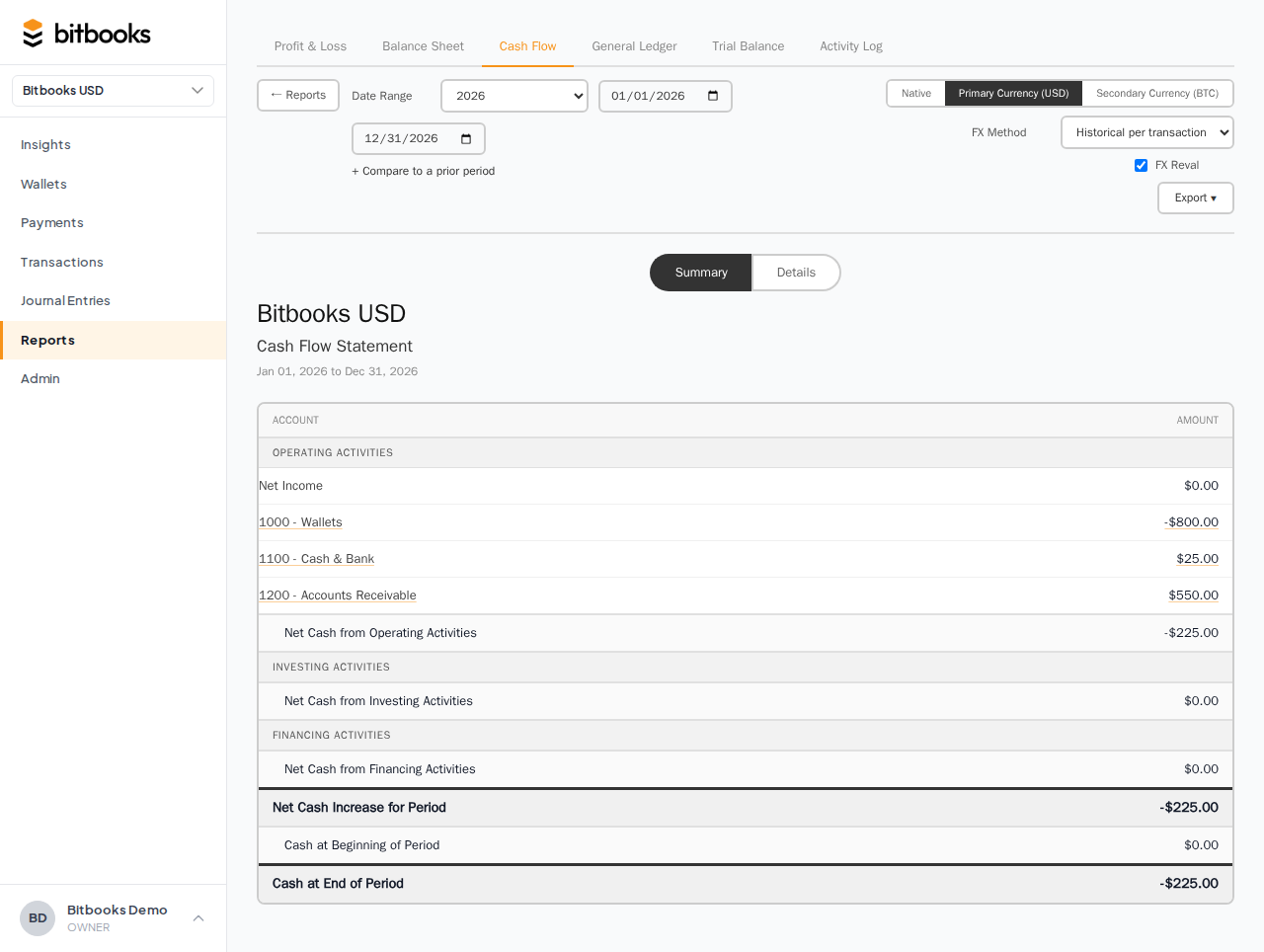

- Click Reports in the left sidebar

- Click Cash Flow tab

- Pick a date range

- The report renders

The three sections

A standard Cash Flow Statement has three sections, in this order:

Operating activities

Cash from running the business: collecting from customers, paying vendors, paying salaries, paying rent.

A typical line list:

Net Profit (from P&L) $12,830

+ Depreciation (non-cash) $1,000

+ Increase in Accounts Payable $2,000

- Increase in Accounts Receivable ($3,500)

- Increase in Inventory ($1,200)

─────────────────────────────────────

Net Cash from Operations $11,130

Operating cash is the most important number. If it's negative, your business is consuming cash from operations and you need other sources (investment, financing) to keep going.

Investing activities

Cash spent or received from investments: buying or selling fixed assets, acquiring or selling Bitcoin as a treasury reserve, buying long-term securities.

Purchase of Office Equipment ($3,000)

Purchase of Bitcoin (treasury) ($50,000)

─────────────────────────────────────

Net Cash from Investing ($53,000)

For most small businesses, this section is small. For Bitcoin treasuries, the Bitcoin acquisition flows here.

Financing activities

Cash from owners or lenders: capital contributions, loan proceeds, dividends paid, loan repayments.

Owner Contribution $25,000

Loan Repayment ($1,500)

─────────────────────────────────────

Net Cash from Financing $23,500

For startups, this section captures investor and founder funding.

The total

Net Cash from Operations $11,130

Net Cash from Investing ($53,000)

Net Cash from Financing $23,500

─────────────────────────────────────

Net Change in Cash ($18,370)

+ Cash at Beginning of Period $80,000

─────────────────────────────────────

Cash at End of Period $61,630

The "Cash at End of Period" should match the actual cash on hand from the Balance Sheet. If it doesn't, something is broken.

Direct vs Indirect method

There are two ways to compute the Operating section:

Direct method

List actual cash receipts and disbursements: cash collected from customers, cash paid to suppliers, cash paid to employees.

Pros: easy to read, intuitive.

Cons: data-heavy, requires tagging every transaction by cash impact.

Indirect method

Start with Net Profit from the P&L, adjust for non-cash items (depreciation, amortization, FX gains/losses) and changes in working capital (receivables, payables, inventory).

Pros: derives from existing P&L and Balance Sheet, less data work.

Cons: less intuitive for non-accountants.

BitBooks uses the indirect method by default. Most accounting tools do; it's the standard.

Why the indirect method makes sense

For a small business, you've already calculated Net Profit. The Cash Flow Statement piggybacks on it: take Net Profit, undo the parts that didn't actually involve cash (like depreciation), and adjust for the timing differences between when revenue/expenses are recognized and when cash actually moves.

The mechanics:

- Add back depreciation: depreciation is an expense on the P&L but no cash actually left

- Adjust for AR changes: if AR went up, customers haven't paid yet, so cash didn't come in

- Adjust for AP changes: if AP went up, vendors haven't been paid yet, so cash didn't go out

- Adjust for inventory: inventory bought is cash out; inventory sold is part of COGS

The result is a cash-only view of operations.

Bitcoin businesses and the Cash Flow Statement

For Bitcoin businesses, "cash" usually means functional currency cash plus settled, non-volatile holdings. Bitcoin treasury holdings are typically classified as Investing activities (a long-term asset, not operating cash).

So:

- Selling Bitcoin: cash inflow from Investing

- Buying Bitcoin (as treasury): cash outflow from Investing

- Operating Bitcoin (Lightning sales for goods/services): part of Operating

This split matters because operating cash is what tells you if your business is sustainable. Treasury moves are separate.

If your business is itself a Bitcoin treasury (your "operations" ARE the Bitcoin holdings), the classifications shift. Talk to your accountant.

Common questions

"My P&L shows a profit but my Cash Flow shows a loss in operations. How?"

Most common reasons:

- Customers haven't paid yet (AR went up)

- You paid for inventory or supplies you haven't sold yet

- A big depreciation expense reduced profit but didn't cost cash

Profit and operating cash diverge in normal businesses. The CF is what surfaces the gap.

"My ending cash on the CF doesn't match my Balance Sheet."

Should match. If it doesn't, run the Trial Balance first to confirm internal consistency. If TB is balanced but CF doesn't tie, contact support.

"Do I need a Cash Flow Statement for a small business?"

Not strictly required, but extremely useful. Lenders, investors, and accountants always ask for it. Even just glancing at it once per quarter is informative.

Where to go next

- Profit & Loss Report for the income statement

- Balance Sheet for the snapshot of assets/liabilities/equity

- General Ledger for transaction-level detail

- Trial Balance for verifying the books are internally consistent

- Tracking Bitcoin Value Changes for how revaluations affect the Cash Flow